Is Nvidia benefitting from permanent demand or a competitive race?

If three customers account for 64% of your receivables, you have the same structural problem Nvidia has. Here’s the financial history lesson that explains why that matters.

There’s a Harvard Business School case study that doesn’t get nearly enough attention outside MBA programs. It’s about a modular housing company called Stirling Homex that collapsed in 1972. The lesson it teaches may be relevant to the current Nvidia story.

Stirling Homex built prefabricated homes. Good product, real demand for affordable housing, Wall Street loved the growth story. One problem: they were booking revenue the moment a unit left the factory – no confirmed buyer, no approved site, no government financing in place. The cash flow statement was a disaster while the income statement looked great. When the banks finally looked closely and called $38.8 million in loans, Stirling Homex couldn’t pay. Out of 10,000 units manufactured, fewer than 1,000 had actually been sold and cash collected. The rest were sitting in open fields, wrapped in plastic.

The HBS lesson: a company can look wildly profitable and still be headed toward a cash flow crunch or even insolvency. Follow the cash, not the income statement.

So what does this have to do with Nvidia?

Investor Michael Burry, famously featured in The Big Short movie, is questioning Nvidia’s growth. He’s saying its revenue growth may be sitting on a sales foundation that the market is pricing as permanent – when it isn’t.

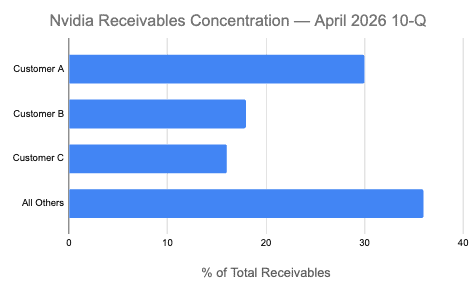

Nvidia’s April 2026 10-Q: three Nvidia customers now account for 64% of total accounts receivable. In 2020 that number was 33%. That change is not insignificant.

Burry is questioning why those three customers are buying at this pace. He calls it the “bezzle” – a term coined by economist John Kenneth Galbraith to describe a period where the illusion of wealth runs rampant, and people believe they own more than actually exists. Burry is saying that a large chunk of current AI chip spending comes from companies benchmarking models, testing systems, and racing each other on AI leaderboards. It does not reflect spending on permanent demand. The competitive sprint is being priced as a permanent market.

His phrase: “They are just flying empty airplanes around.”

That’s the Stirling Homex problem in different form. The chips are real. The manufacturing capacity is real. The question is whether the demand is permanent.

The balanced read: the bear case isn’t that AI is fake. It’s that three customers control 64% of receivables, and if their capital allocation priorities shift – even partially – the revenue hole is immediate and large.

What business operators should actually take from this

Most of the Nvidia coverage is written for investors. Here’s what matters if you run a $1M–$100M business.

Concentration risk is not just a big-company problem. If it unwinds, the cash flow catch-up at $20M of sales is just as brutal proportionally as it is at $50B revenue. You can run a proactive audit on your own risk profile using our dedicated Customer Concentration Risk Prompts.

Watch what your vendors’ financials and actions tell you. The red flags Stirling Homex showed – revenue growing while operating cash flow turns negative, receivables ballooning faster than collections, costs being capitalized to keep earnings clean – show up in vendor statements, and in your own days-receivables when growth is being funded by deferred collections rather than actual cash.

Be skeptical of infrastructure spending dressed up as demand. Right now every AI tool vendor is pricing their product as if the hyperscaler buildout represents permanent, growing end-user demand. It may. It may not. Before you lock into anything long-term, ask the same question Burry is asking about Nvidia: is this real cash-paying demand, or is someone flying empty airplanes?

Bottom line

Nvidia builds real technology. The bear case isn’t that the chips don’t work. It’s a question of how durable the demand is, and what happens when three customers represent 64% of your receivables and one of them blinks.

History runs this outcome on a loop:

The Telecom Fiber Glut (1990s): Telecom giants laid over $500 billion in fiber infrastructure built on the assumption of permanent growth. Only 3% of the fiber they laid was ever needed to meet actual consumer demand. The rest sat dark for a decade.

The Radio Boom (1920s): RCA became the ultimate glamour stock as broadcasting infrastructure surged. The stock ran from under $5 to over $540 at its peak. Once the industry infrastructure was built out, and with the help of the 1929 crash, 98% of that value was wiped out.

Stirling Homex (1972): 10,000 units manufactured. Fewer than 1,000 paid for. The rest wrapped in plastic in empty fields.

Exceptions exist. Tesla’s early Gigafactory and Supercharger buildout is the clearest counterexample – infrastructure spend that created durable, cash-generating consumer demand. But Tesla was building for a market that needed physical infrastructure to exist at all. The hyperscalers are building for a market that may already be served at a fraction of planned capacity once the benchmarking race ends.

The pattern isn’t that infrastructure investment is always wrong. It’s that a frantic corporate race to out-build competitors gets repeatedly mistaken for permanent end-user demand – and the cash flow catch-up when it arrives is brutal.

Maybe this time it’s different.

For business operators: the analytical discipline that would have spotted Stirling Homex in 1971 is the same one that protects your business today. Follow the cash. Question demand permanence. Know your customer concentration.

If you are preparing for a future exit or trying to de-risk your operations, use our structured Competitive Strategy framework to build an unassailable strategic moat.

Are you tracking your own customer concentration the same way you’d read Nvidia’s 10-Q?

Econblox provides AI-powered business advisory tools for business operators running $1M–$100M businesses. econblox.com

No Credit Card Required For Trial

No Credit Card Required For Trial