Working capital is the lifeblood of any growing business. For mid-market companies generating between $5 million and $100 million in annual revenue, effective working capital management can mean the difference between seizing growth opportunities and struggling with cash flow constraints.

Working capital, defined as current assets minus current liabilities, reflects a company’s operational liquidity. A National Center for the Middle Market survey of 400 C-suite executives found that mid-market firms are typically tying up tens of millions of dollars in less-than-optimal working capital practices, and in some cases more than $100 million. This article explores the core components, common challenges, and actionable tactics that mid-market leaders can use to strengthen their working capital position.

The Importance of Working Capital Management in the Mid-Market

Mid-market businesses operate in a unique space. They are large enough to have complex operations but often lack the dedicated treasury functions of a large enterprise. Strong working capital management helps these companies mitigate supply chain disruptions, reduce reliance on costly short-term financing, and enhance supplier relationships. By improving cash conversion cycles, mid-market firms can unlock cash that would otherwise be tied up in receivables, payables, and inventory. This cash can then be reinvested into growth initiatives, technology upgrades, or strategic acquisitions without adding debt.

Core Components of Working Capital Management

Working capital management rests on four core components: accounts receivable management, accounts payable management, inventory management, and cash management. Each component requires focused attention and discipline.

Accounts Receivable Management

Accounts receivable represents money owed to the business by customers. Accelerating the collection of receivables is a primary goal. Tactics include offering early payment discounts to customers, sending timely invoices, and enforcing clear credit terms. The faster cash is collected, the shorter the cash conversion cycle.

Accounts Payable Management

Accounts payable is money the business owes to suppliers. Tightening accounts payable means strategically extending payment terms without damaging supplier relationships. Negotiating favorable payment terms with vendors is a best practice that many mid-market companies overlook. Paying invoices exactly when they are due, rather than early, preserves cash for longer.

Inventory Management

Excess inventory ties up cash and increases storage costs. Mid-market businesses must balance having enough stock to meet demand without overstocking. Techniques such as just-in-time inventory, demand forecasting, and regular turnover analysis help optimize inventory levels.

Cash Management

Accurate cash flow forecasting is critical for managing working capital. Cash management involves monitoring daily cash positions, projecting future inflows and outflows, and ensuring sufficient liquidity to cover obligations. Technology and automation, such as digitized invoicing and predictive analytics, significantly improve cash management accuracy.

Key Challenges Mid-Size Businesses Face

Mid-market companies encounter specific obstacles when trying to optimize working capital. These challenges include complex operations, limited resources, supplier and customer dependence, cash flow volatility, lack of technology, and risk aversion. Unlike large corporations with dedicated treasury teams, mid-market financial leaders often wear multiple hats, making it difficult to focus on working capital improvement. Dependence on a few large customers or suppliers can also create vulnerability, echoing the same customer concentration risk and vendor dependency risk that show up elsewhere in a company’s financial profile. Cash flow volatility, particularly in seasonal or cyclical industries, adds another layer of difficulty. Many mid-market firms also lag in adopting financial technology, relying on spreadsheets instead of automated systems.

Actionable Tactics to Improve Working Capital

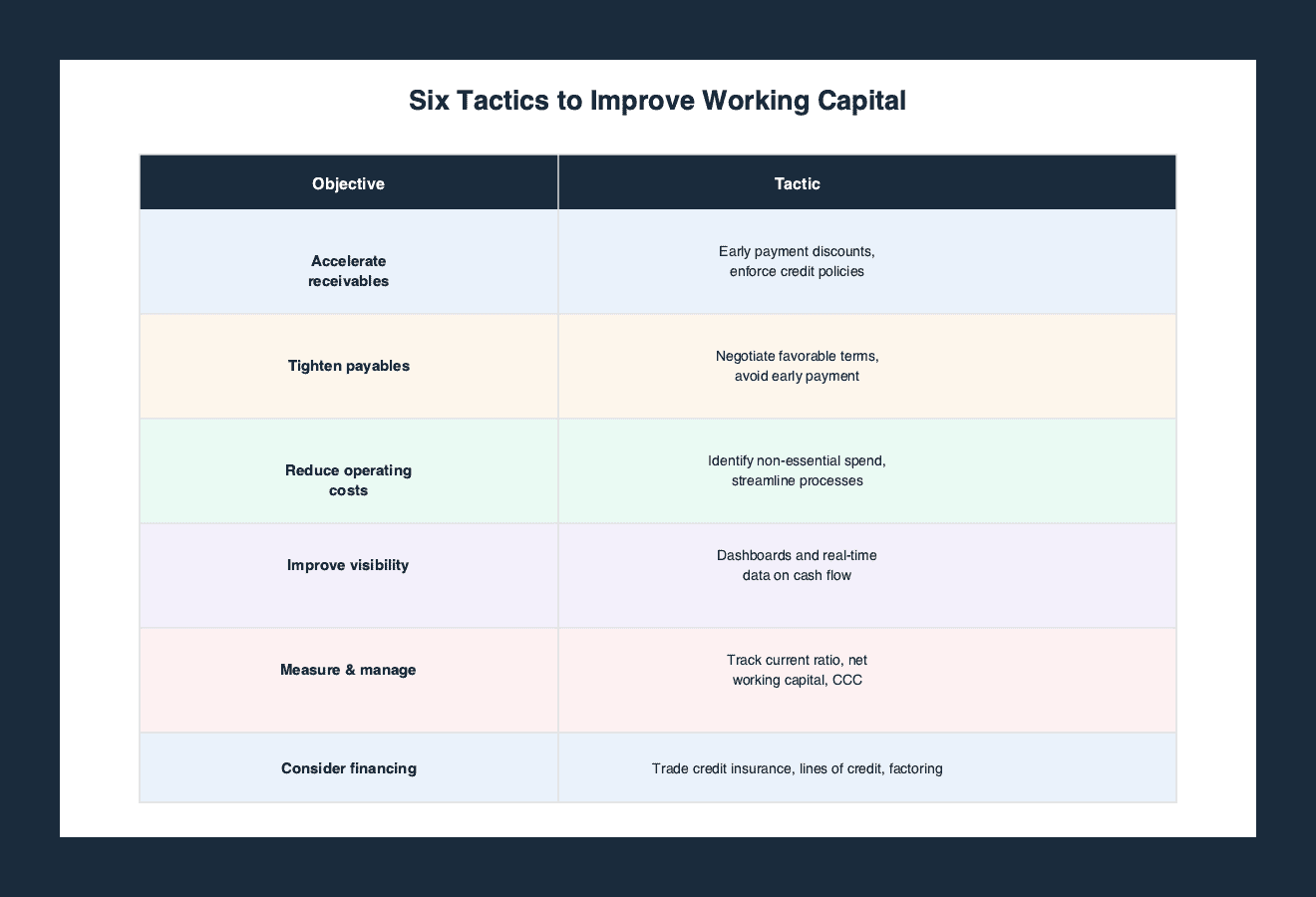

The table below summarizes the tactics business owners can use to improve their working capital.

| Objective | Tactic |

|---|---|

| Accelerate accounts receivable | Offer early payment discounts to customers, enforce credit policies |

| Tighten accounts payable | Negotiate favorable payment terms with suppliers, avoid early payment |

| Reduce operating costs | Identify non-essential expenses, streamline processes |

| Improve visibility and controls | Use dashboards and real-time data to monitor cash flow |

| Measure and manage working capital | Track KPIs like current ratio, net working capital, cash conversion cycle |

| Consider financing options | Use trade credit insurance, lines of credit, or factoring |

Trade credit insurance is one financing-related tool that protects against non-payment, helping mid-market companies extend credit to customers with greater confidence. However, not every business needs this tool; the decision depends on customer credit risk profiles.

Measuring and Monitoring Working Capital Performance

To improve working capital, companies must measure it. Key ratios include the current ratio, with a target range of 1.2 to 2.0, and net working capital, which is simply current assets minus current liabilities.

Another critical metric is the cash conversion cycle, which measures how long cash is tied up in operations from the time inventory is purchased to when receivables are collected. Because working capital efficiency feeds directly into cash flow and profitability, it also factors into how a business is valued on an EBITDA multiple basis.

Monitoring these metrics monthly or quarterly allows management to spot trends and take corrective action. The National Center for the Middle Market survey highlighted that many mid-market executives see significant room for improvement in these areas, yet few have formal working capital programs in place.

The Role of Technology and Automation

Technology is a key enabler for working capital management. Digitized invoicing, automated payment reminders, and predictive analytics can reduce manual effort and error. Improving visibility and controls through technology helps mid-market companies react faster to cash flow changes.

Automation and predictive tools can help optimize inventory levels and forecast cash needs more accurately. For companies with limited resources, adopting one or two technology upgrades, such as an automated accounts receivable platform, can deliver immediate returns. Tools like Econblox’s AI-powered business advisor can help track these metrics on an ongoing basis alongside the rest of a company’s financial picture.

By systematically applying these tactics and leveraging technology, mid-market businesses can reduce their reliance on costly short-term financing, strengthen supplier relationships, and build a more resilient financial foundation. Effective working capital management can unlock significant cash that fuels strategic growth.

Frequently Asked Questions

What is the ideal current ratio for a mid-market business?

A current ratio between 1.2 and 2.0 is generally considered healthy for most mid-market companies. A ratio below 1.0 indicates potential liquidity issues, while a ratio above 2.0 may suggest too much cash tied up in assets. The appropriate target depends on industry and business cycle.

How can a mid-market company improve its cash conversion cycle?

Improving the cash conversion cycle requires accelerating accounts receivable through early payment discounts and stricter credit terms, negotiating longer payment terms with suppliers, and reducing excess inventory. Regular monitoring of days-sales outstanding and days-payable outstanding helps identify bottlenecks.

What is the difference between working capital and net working capital?

Working capital is calculated as current assets minus current liabilities. Net working capital is the same figure but often adjusted for cash and debt to reflect only operational liquidity. Some analysts use net working capital to exclude non-operating items like cash and marketable securities.

Should a mid-market business use trade credit insurance?

Trade credit insurance protects against customer non-payment, which can stabilize cash flow and allow a business to extend credit more confidently. It is most useful for companies with a few large customers or those exporting to unfamiliar markets. It is not standard in all mid-market businesses.

Working capital management is not a one-time project but an ongoing discipline. By focusing on the four core components, addressing mid-market specific challenges, leveraging technology, and applying proven tactics, business leaders can improve their company’s financial health and position it for sustained growth. Optimizing cash cycles is the single most important safeguard to avoid the deadly growth trap business cash flow pattern. Failing to project cash flow gaps leads straight into a painful overspending trap scaling business situation. Maintaining adequate liquidity should always be priority one for your capital allocation strategies mid-market checklist.

No Credit Card Required For Trial

No Credit Card Required For Trial