The traditional 60/40 balanced portfolio has been a cornerstone of investment strategy for more than seven decades. The concept is straightforward: 60% in equities for growth and 40% in bonds for stability. For a long time, this mix delivered reliable, risk-adjusted returns for investors. But recent market conditions have led many experts to question whether this classic allocation can still deliver going forward. The debate intensified after 2022, when both stocks and bonds posted negative returns in the same calendar year, a shared decline of a kind not seen since the high-inflation years of the late 1960s and 1970s.

What Is the 60/40 Portfolio and Why Did It Work for Decades?

The 60/40 portfolio originates from Harry Markowitz’s Modern Portfolio Theory, introduced in 1952. The idea relies on the historical negative correlation between stocks and bonds. When equities fall, bonds often rise as investors seek safety, cushioning the overall portfolio’s decline. Bonds also provide regular income and lower volatility. Over the decades, this relationship held consistently enough that the 60/40 became the default recommendation for a “balanced” investor.

For business owners, the 60/40 portfolio was particularly attractive. It allowed them to grow capital while maintaining a buffer against market shocks. The strategy required little maintenance and seemed to work in almost any environment, until it didn’t.

The 2022 Reality Check: When Both Stocks and Bonds Fall

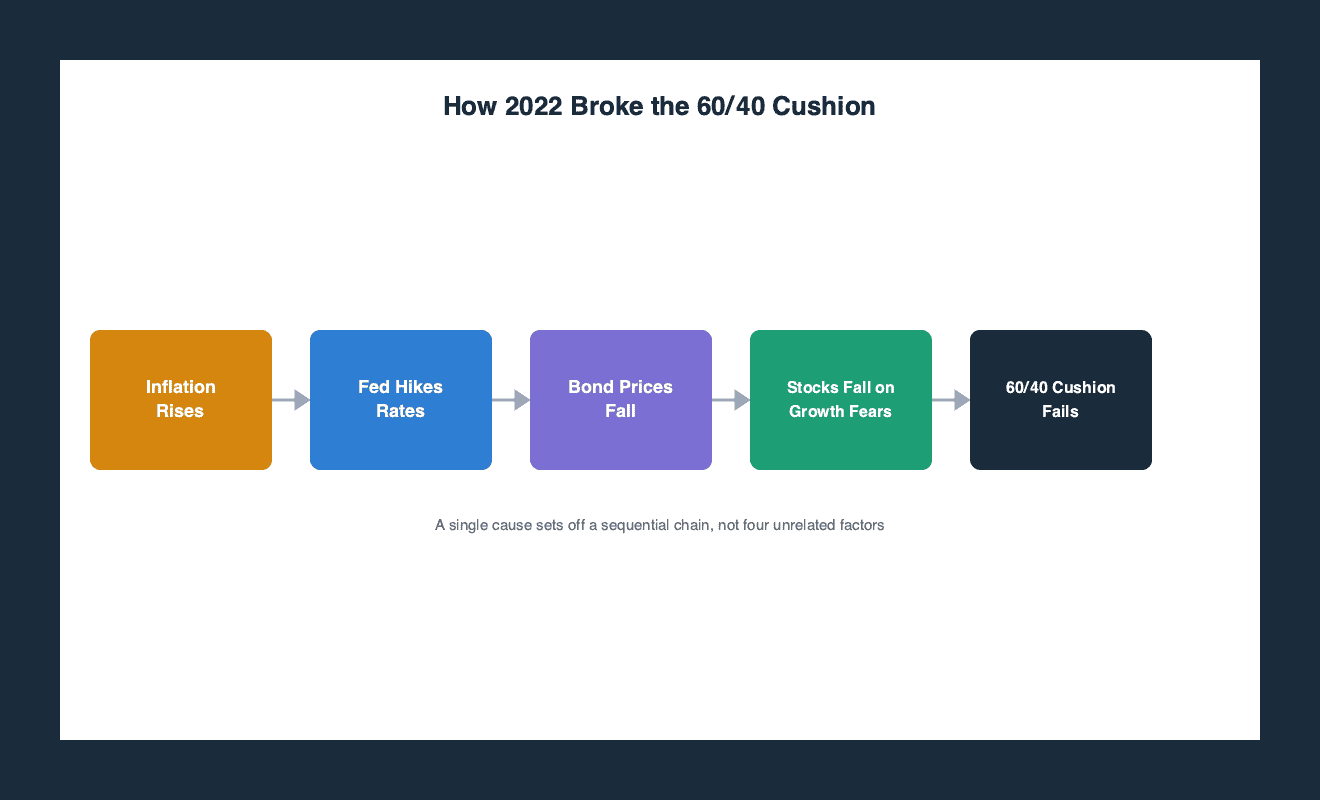

The relationship between stocks and bonds broke down in 2022. For the first time in decades, both asset classes fell in tandem. The primary driver was rising inflation, which prompted the Federal Reserve to raise interest rates aggressively. Bonds, which are highly sensitive to interest rate changes, lost value. At the same time, equity markets declined on fears of a slowing economy. The traditional hedge failed, and a 60/40 portfolio suffered losses that surprised many investors.

The old assumptions about bond performance may no longer hold. A year in which both stocks and bonds post negative returns is historically uncommon, and 2022 was one of them. That rarity does not make the event less painful for those who relied on the 60/40 model.

Why Some Experts Say the 60/40 Portfolio Is Broken

Skepticism about the 60/40 model is not new. Bob Rice, Chief Investment Strategist at Tangent Capital, warned as early as 2015 that a 60/40 portfolio was on track to grow only around 2.2% per year going forward, arguing that “the things that drove 60/40 portfolios to work are broken” and that stocks and bonds alone could no longer deliver what clients wanted. That warning predates the 2022 downturn by years, but it captured a concern that resurfaced with new force once bonds actually failed to cushion a stock decline.

More recently, Louis Gave, founding partner at Gavekal, has argued in a recorded interview that the 60/40 portfolio effectively died during COVID and that bonds no longer serve their traditional safe-haven role. Gave has pointed to energy stocks as a potential replacement for bonds in a portfolio.

The Counterargument: Not Broken, Just Needs Improvement

Not everyone agrees that the 60/40 portfolio is beyond repair. Russell Investments argued that the portfolio is “not forever” broken and expects it to revive under different macroeconomic conditions, citing easing inflationary pressures and central banks nearing the end of their tightening cycles. Their view suggests that the relationship between stocks and bonds is cyclical, not permanently severed. When inflation moderates and interest rates stabilize, bonds may again provide the diversification they once did.

Jason Kephart of Morningstar takes a middle position. He describes a “total portfolio approach” that groups investments by risk role, typically a growth sleeve and a stability sleeve, rather than fixed percentage allocations. Under this method, investors classify assets by what they contribute to the portfolio, such as growth or stability during downturns, and adjust accordingly. Kephart’s approach acknowledges that the old formula may need refinement without abandoning stocks and bonds entirely.

For business owners evaluating their strategy, the question is not simply whether the 60/40 is dead, but whether they can adapt it to a world where inflation and interest rate cycles are less predictable.

Alternative Portfolio Allocations to Consider

Given the uncertainty around the 60/40, several alternatives have been proposed. These may not be suitable for every investor, but they reflect the range of thinking among leading institutions and strategists.

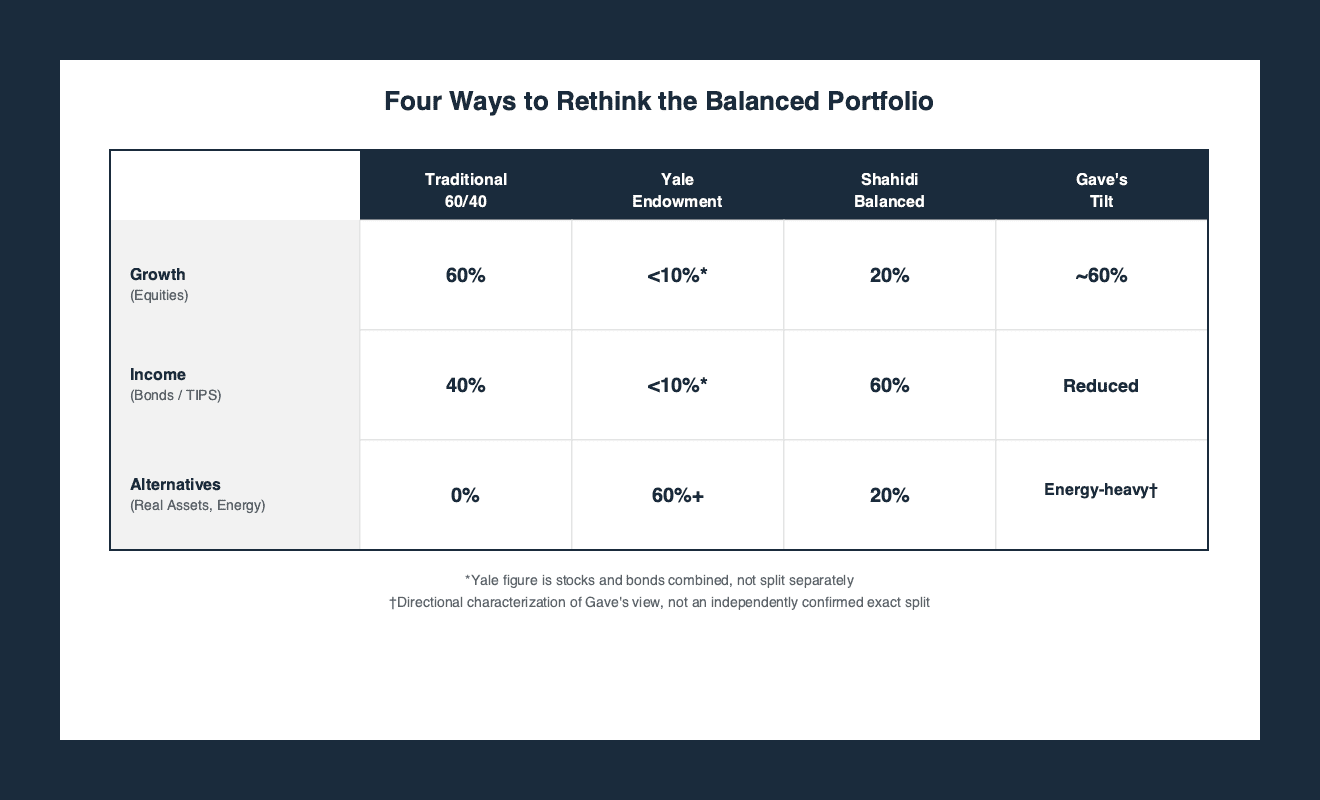

- Yale University’s endowment model. Yale allocates more than 60% of its endowment to alternative assets such as venture capital, real estate, and natural resources, with traditional domestic stocks and bonds combined making up less than 10% of the portfolio. This allocation has produced strong long-term results but is not easily replicated by individual investors due to liquidity and minimum investment requirements.

- Alex Shahidi’s balanced asset allocation model. Shahidi, author of Balanced Asset Allocation (2014), outlined a portfolio of roughly 30% long-term Treasury bonds, 30% Treasury Inflation-Protected Securities (TIPS), 20% equities, and 20% commodities. He argued that this combination can yield returns comparable to a 60/40 portfolio with less volatility, especially during inflationary periods. Since 2014, such a portfolio did deliver less volatility but the overall return was less than the 60/40 portfolio.

- Louis Gave’s energy-for-bonds thesis. As noted above, Gave has argued for reducing reliance on bonds and adding exposure to energy stocks and precious metals.

- Morningstar’s total portfolio approach. Rather than prescribing specific percentages, Jason Kephart suggests building a portfolio around risk roles, growth assets and stability assets, with the exact mix changing as market conditions evolve.

Russell Investments, for its part, continues to recommend a version of the 60/40, suggesting that investors should not abandon the strategy entirely but may need to adjust expectations. For business owners who manage both corporate and personal assets, evaluating these alternatives requires a clear understanding of their cash flow needs, investment horizon, and risk tolerance.

Frequently Asked Questions

Is the 60/40 portfolio completely dead?

There is significant disagreement among experts. Louis Gave argues it effectively died during COVID, while Russell Investments believes it can revive under different conditions. Morningstar says it is not broken but can be improved. The answer depends on your investment horizon, risk tolerance, and expectations for inflation and interest rates.

Can individual investors replicate Yale University’s endowment allocation?

Yale’s endowment holds well over 60% in alternative assets. That approach typically requires large minimum investments, long lock-up periods, and access to top-tier private equity managers. Most individual investors cannot directly replicate it, but they can incorporate some alternative assets through publicly traded real estate investment trusts, commodity ETFs, or managed futures. Ask your financial advisor.

What is the “total portfolio approach” recommended by Morningstar?

Jason Kephart of Morningstar suggests classifying each investment by its risk role, such as growth or stability, rather than sticking to a fixed percentage like 60/40. Investors then adjust the mix based on current market conditions and their personal goals. This approach aims to improve the portfolio’s resilience without abandoning stocks and bonds entirely.

Should I sell all my bonds and buy energy stocks instead?

Some strategists have floated energy stocks as a partial bond replacement. However, this is a specific view from individual commentators, not a consensus. Bonds still serve a purpose in many portfolios, especially for investors seeking income and lower volatility. Before making such a shift, consider your time horizon and consult a financial advisor to evaluate the risks.

The debate over the 60/40 portfolio reflects a broader uncertainty about the future relationship between stocks and bonds. For business owners, this uncertainty has real consequences for both corporate treasury management and personal retirement planning.

No single alternative has emerged as the clear successor, but the range of proposals, from Yale’s heavy tilt into alternatives to Shahidi’s inflation-focused mix, provides a starting point for rethinking the classic balanced portfolio. Investors should weigh the conflicting expert opinions including their own financial advisor’s opinion, consider their own goals, and remain open to adjusting their approach as economic conditions evolve. Assuming historic correlation models still protect your capital is among the most dangerous retirement plan warning signs in today’s fiscal environment. For business owners, the portfolio question is compounded by the fact that many operate on a business owner retirement pension model — making the business itself the largest and most illiquid asset in their retirement picture. When traditional portfolios underperform, a peak-value business exit becomes the most powerful wealth engine available, making a clear understanding of your business valuation for owners an essential starting point.

No Credit Card Required For Trial

No Credit Card Required For Trial