Most retirement savers watch their 401(k) balances monthly and worry about stock market dips. But a much slower, quieter threat is eating away at purchasing power, long-term growth, and the stability of programs like Social Security. That threat is the growing pile of U.S. government debt. While the debt ceiling debates, deficit spending, and bond yields may seem remote from your personal savings, the connection is direct and compounding. Understanding how federal borrowing affects your retirement is no longer optional for anyone planning a secure financial future.

The Link Between Government Debt and Your Nest Egg

Government debt shapes the economic environment in which your retirement savings grow or shrink. When the federal government borrows heavily, it competes for capital, which can push interest rates higher. Higher rates reduce the value of existing bonds in your portfolio and can slow economic activity, hurting corporate earnings and stock prices. More importantly, large debt loads often lead to inflationary pressures as the government may be tempted to monetize its obligations. An Allianz Life consumer survey summarizes the problem simply, “Debt can have a significant impact on achieving long-term financial goals like retirement.” The cumulative effect is a slow drain on the real value of every dollar you save.

How the Debt Ceiling Creates Ripple Effects

The debt ceiling is an artificial limit on how much the U.S. Treasury can borrow. When the government approaches that limit, political standoffs can create uncertainty that rattles markets. On July 4, 2025, President Trump signed the One Big Beautiful Act into law which again raised the debt ceiling so that federal deficit spending could continue, increasing the possibility of government default. The very possibility of a default can cause stock market volatility and spike borrowing costs. For retirement savers, this means unpredictable swings in portfolio values and potential losses as government deficit spending continues. The uncertainty itself is damaging, as it undermines confidence in the long-term stability of government-backed securities that anchor many retirement portfolios.

Inflation and the Erosion of Purchasing Power

One of the most direct channels through which government debt damages retirement savings is inflation. Persistent deficit spending can overheat the economy or force the Federal Reserve to keep interest rates higher for longer. Both scenarios erode the purchasing power of fixed-income savers and those relying on cash-like assets. Inflation is particularly insidious because it compounds quietly. A dollar saved today may buy noticeably less in twenty years, especially if debt-driven inflation runs above historical averages. Understanding how the debt limit lift impacts your retirement savings is key to protecting yourself from this hidden tax on your nest egg.

Social Security’s Role in the Debt Debate

Social Security is often brought up in conversations about the national debt, but the relationship is not a simple cause and effect. Social Security can run a short-run deficit only if it has previously run surpluses, since the program is barred from borrowing and must balance its budget over the long run. The program is currently drawing down trust fund assets to pay for the Baby Boomer generation. While Social Security does not directly cause the federal deficit, the broader budget situation affects the political will to shore up the program. If government debt continues to grow, lawmakers are going to be less inclined to increase Social Security benefits and more inclined to consider benefit cuts or eligibility changes. For retirees who depend on those payments, this uncertainty adds another layer of risk to their planning.

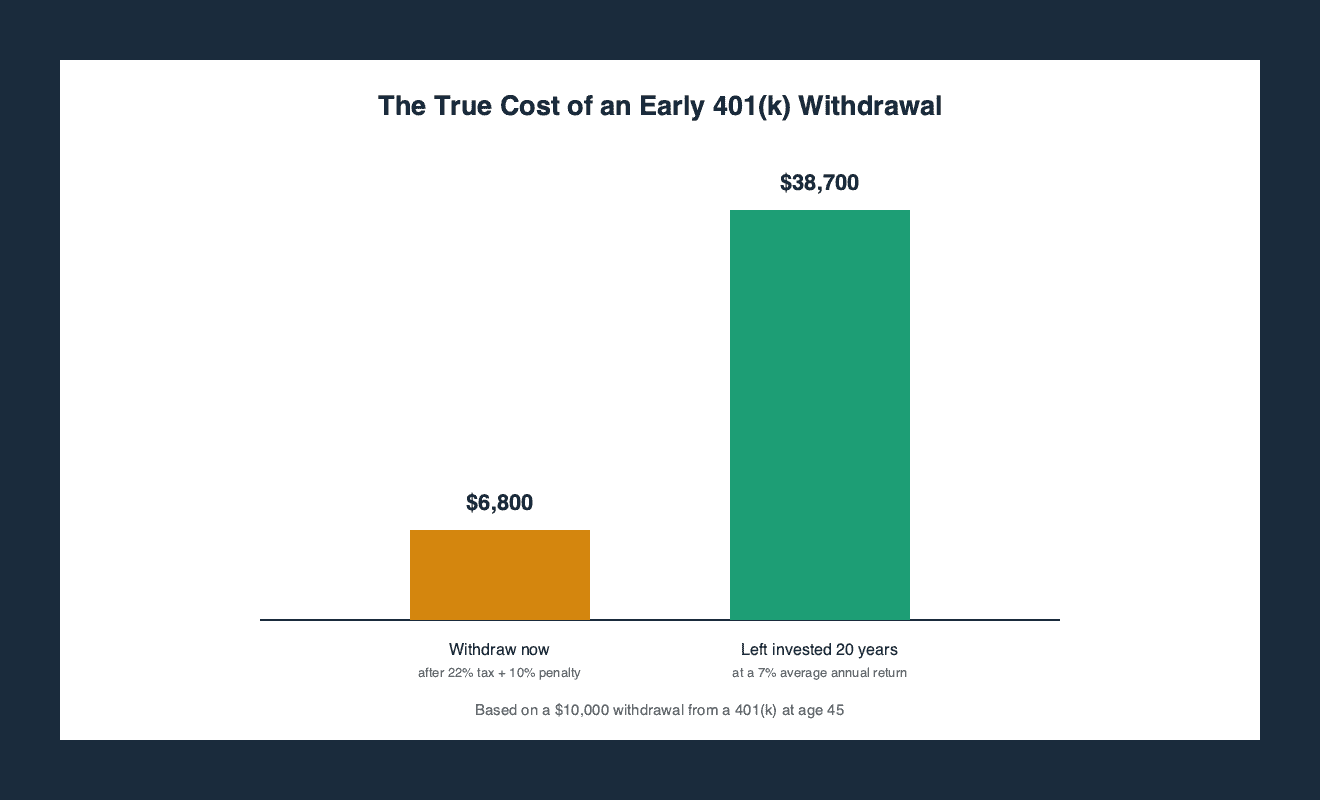

The Danger of Using Retirement Savings to Pay Debt

When faced with high personal debt, some individuals consider raiding their retirement accounts. The logic seems straightforward: pay off expensive credit card debt or a car loan using the money in your 401(k) or IRA. But the costs can be steep. Using retirement savings to pay down debt may cost you more than it helps, with the potential for taxes, penalties, and lost investment growth. Early withdrawals are subject to income tax plus a 10% penalty in most cases, and the money you take out will never compound again. Even if you intend to repay it, the opportunity cost of missing market gains can be substantial over time. Government debt may be straining your budget through higher inflation and interest rates, but dipping into retirement funds is rarely the solution.

How Consumer Debt Compounds the Problem

Government debt can indirectly make your personal debt more expensive and harder to escape. When the Treasury borrows heavily, it can push up interest rates on everything from mortgages to credit cards. Monthly payments toward high-interest consumer debt can divert money away from retirement accounts, reducing long-term savings and financial progress. The burden of carrying that debt means you contribute less to your 401(k) or IRA each year. Over a career, those missing contributions can snowball into a significant shortfall. The connection between federal borrowing and your personal interest rates may not be obvious month to month, but over decades it can be devastating to your retirement readiness.

What You Can Do to Protect Your Retirement

While you cannot control government borrowing, you can strengthen your position against its effects. Focus on paying down high-interest personal debt to free up cash for retirement contributions. Maintain a diversified portfolio that includes inflation-protected securities, international equities, and real assets that can weather rising rate and inflation environments. Stay informed about fiscal policy and debt ceiling debates so you can adjust your strategy before markets react. The key is to build resilience into your plan, recognizing that government debt will likely remain a persistent drag on economic growth and purchasing power for years to come.

Frequently Asked Questions

How does government debt affect my 401(k) balance?

Rising government debt can lead to higher interest rates and inflation, which may reduce the value of bonds in your portfolio and slow economic growth that supports stock prices. The uncertainty of debt ceiling battles can also cause short-term market volatility that temporarily lowers your account balance.

Should I cash out my retirement savings to pay off personal debt?

Using retirement savings to pay debt may cost you more than it helps, with the potential for taxes, penalties, and lost investment growth. Early withdrawals are taxed as income and often carry a 10% penalty, and you forfeit future compounding on that money.

Can Social Security be cut because of the national debt?

Social Security is funded by payroll taxes and trust fund reserves, not directly by the federal budget. However, growing government debt may reduce political willingness to strengthen the program, increasing the risk of future benefit cuts or eligibility changes.

What is the debt ceiling and why does it matter for retirement?

The debt ceiling is a legal limit on how much the U.S. Treasury can borrow. When political fights delay raising it, the risk of default rises, which can cause stock market drops and higher borrowing costs that hurt retirement portfolios.

How does inflation from government debt hurt my savings?

Inflation reduces the purchasing power of every dollar saved. If government debt drives sustained higher inflation, the real value of your nest egg declines even if your nominal balance grows. Fixed-income savers are especially vulnerable because their returns may not keep pace.

Government debt is not a distant policy concern, it is a real and ongoing factor in the health of your retirement savings. By understanding the channels through which federal borrowing affects inflation, interest rates, Social Security, and your own personal finances, you and your financial advisor can discuss which proactive steps can help you protect your future. In this environment, the traditional 60/40 portfolio broken assumption deserves serious re-examination. Business owners face an additional layer of exposure — for those running on a business owner retirement pension model, the macro forces described here compound against the illiquidity of their primary asset. Watch for the key retirement plan warning signs that indicate your current strategy was not built for this fiscal environment. For business owners, optimizing your exit multiple is the most direct path to protecting retirement wealth — start with a clear understanding of your business valuation for owners. And before you can protect margin at the personal level, you need to protect it at the business level — including your ability to raise prices without losing customers.

No Credit Card Required For Trial

No Credit Card Required For Trial