The EBITDA multiple is one of the most frequently used metrics in business valuation. It helps buyers, sellers, and investors quickly compare companies of different sizes and capital structures. Yet the math behind it often seems more complicated than it really is. This article walks through the EBITDA multiple calculation in clear, step-by-step terms, using only the formulas and data that finance professionals actually rely on.

Understanding EBITDA: The First Step

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. According to the Corporate Finance Institute, the standard formula is:

EBITDA = Earnings Before Tax + Interest + Depreciation + Amortization

This figure strips out financing decisions (interest), tax environments, and non-cash accounting charges (depreciation and amortization). The result is a rough proxy for the cash a business generates from its core operations. Because EBITDA is a non-GAAP measure, companies may calculate it slightly differently, so always check the footnotes of a financial statement.

It helps to distinguish EBITDA from two related terms. EBIT (Earnings Before Interest and Tax) excludes only interest and tax. EBITDA goes one step further by adding back depreciation and amortization, giving a clearer view of operating cash performance. For smaller businesses, owners often use Seller’s Discretionary Earnings (SDE), which adds back the owner’s salary and discretionary expenses to net profit. SDE is tailored for small businesses, while EBITDA is more common for larger corporations.

What Is an EBITDA Multiple?

An EBITDA multiple expresses the relationship between a company’s total value and its EBITDA. There are two common forms:

- EV/EBITDA: Enterprise Value divided by EBITDA. This is the more widely used multiple for valuation comparisons.

- EBITDA/EV: EBITDA divided by Enterprise Value. This is the reciprocal, and it measures the cash return on investment relative to enterprise value.

Enterprise Value (EV) itself is calculated as: market capitalization + value of debt + minority interest + preferred shares, minus cash and cash equivalents. This formula captures the full price an acquirer would pay to take over the business, including its debt obligations and excluding its cash.

Because EBITDA/EV is simply the inverse of EV/EBITDA, a higher EBITDA/EV means more operating cash generated for every dollar of enterprise value, which points to a cheaper or more cash-productive business. The EV/EBITDA version is the one most commonly used in valuation and benchmarking.

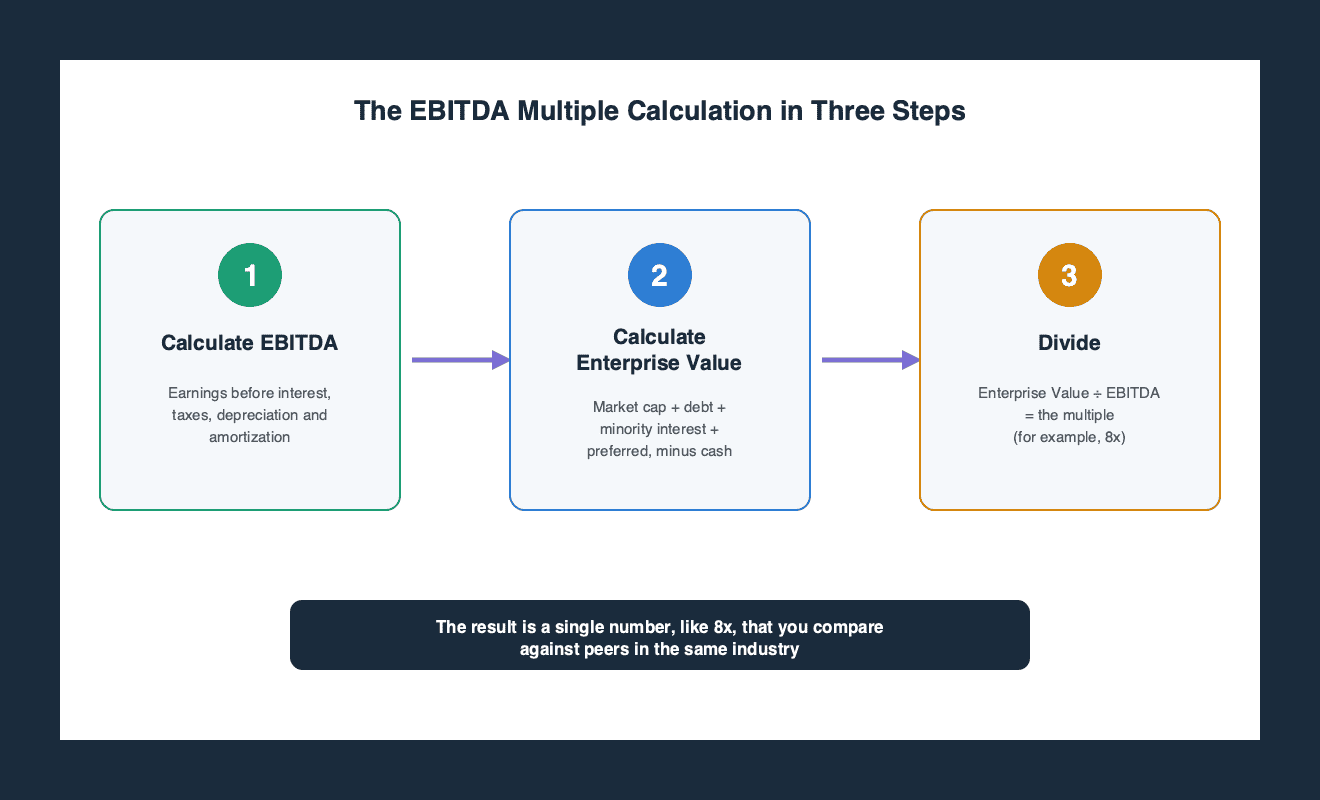

How to Calculate the EBITDA Multiple

Calculating an EBITDA multiple requires just two numbers: Enterprise Value and EBITDA. The core formula is:

EBITDA Multiple = Enterprise Value ÷ EBITDA

To walk through the process in plain terms:

- Calculate EBITDA for the trailing twelve months or a forward period. Use the formula above with actual financial statement figures. For a trailing period, you may need to calculate Last Twelve Months (LTM) EBITDA by adding the most recent stub period’s EBITDA to the latest full-year EBITDA, then subtracting the EBITDA from the corresponding prior stub period. This method, described by Macabacus, avoids double-counting.

- Calculate Enterprise Value. Start with market capitalization (for public companies) or an estimated equity value for private firms. Add total debt, minority interest, and preferred shares. Subtract cash and cash equivalents. For a private company, market capitalization is often replaced by an estimated fair market value of equity.

- Divide. Take the enterprise value you computed and divide it by the EBITDA figure from step one. The result is the multiple, expressed as a number (e.g., 8x).

If you prefer the inverse calculation (EBITDA/EV), simply swap the numerator and denominator: EBITDA divided by Enterprise Value. This yields a percentage that represents the cash return on enterprise value.

Historical vs. Forward Multiples

Analysts calculate EBITDA multiples using either past or future earnings. A historical multiple uses actual EBITDA from the most recent completed fiscal year or trailing twelve months. A forward multiple uses forecasted EBITDA for the coming year or years.

According to the Corporate Finance Institute, forward-looking multiples are usually lower than backward-looking multiples if EBITDA is expected to grow. That makes sense: if future EBITDA is higher, dividing the same enterprise value by a larger number produces a smaller multiple. When comparing companies, it is important to use consistent time periods, historical against historical or forward against forward, to avoid misleading conclusions.

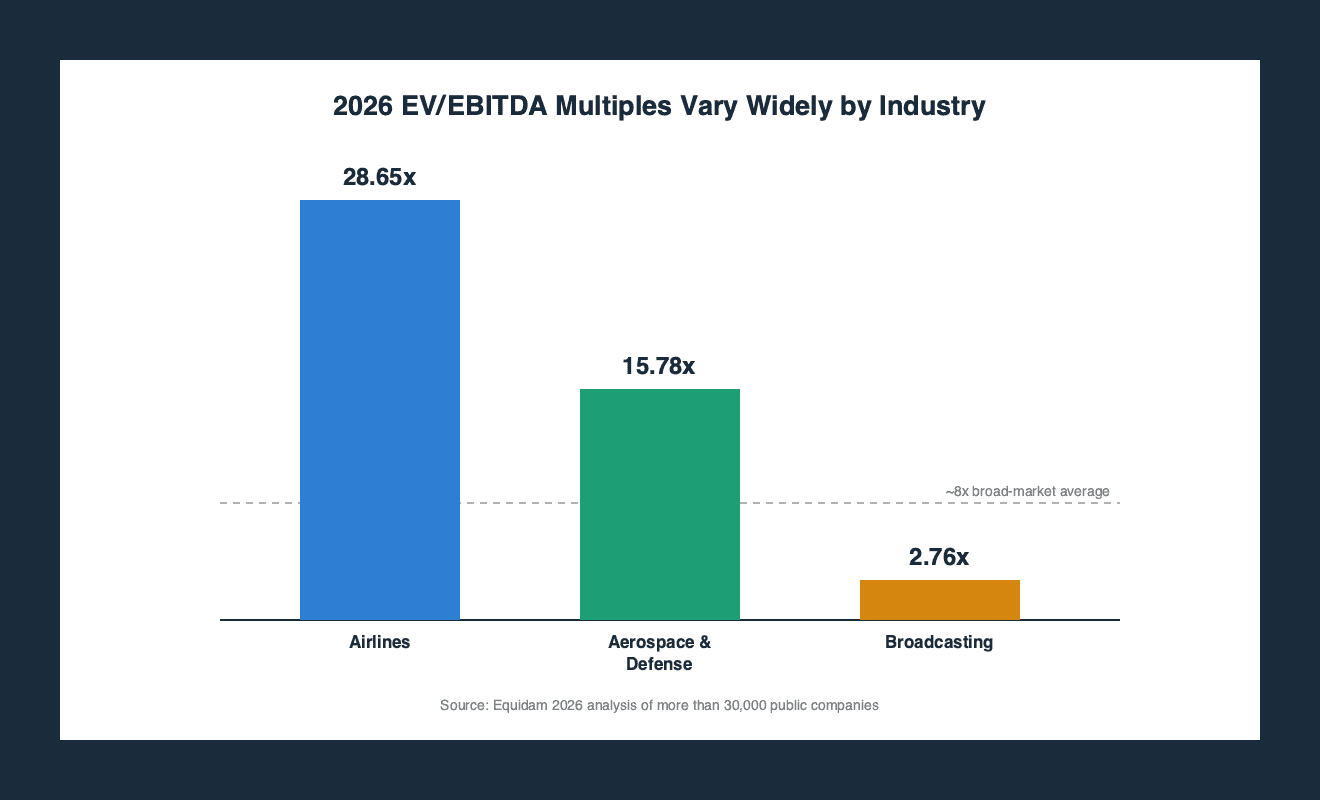

Industry Benchmarks for EBITDA Multiples

No single EBITDA multiple is universally good or bad. The appropriate range depends heavily on industry, company size, growth prospects, profitability and timing in industry profit cycle. The Corporate Finance Institute notes that an EV/EBITDA of about 8x can be considered a broad average for some public companies. However, Equidam’s 2026 analysis of more than 30,000 public companies reveals wide variation:

| Industry | EV/EBITDA Multiple (2026) |

|---|---|

| Aerospace & Defense | 15.78x |

| Airlines | 28.65x |

| Broadcasting | 2.76x |

These figures show that a multiple considered normal in one sector could be extremely high or low in another, at that point in time. When valuing a business, always compare against peers in the same industry and adjust for company-specific factors. Buyers do the same in reverse, applying discounts for the specific risks that lower a purchase price, such as a slow growth rate or thin profit margins.

EBITDA Multiple in Context: SDE and EBIT

Because EBITDA is most relevant for larger companies, small business owners often encounter SDE multiples instead. SDE adds back the owner’s salary and discretionary expenses, making it more appropriate for businesses where the owner’s compensation significantly affects net profit. EBIT, meanwhile, may be used in industries with heavy capital expenditures where depreciation and amortization are meaningful. Understanding which earnings metric to use is crucial because each produces a different multiple and a different valuation result.

When calculating your own EBITDA multiple, be aware that adjustments for unusual or non-recurring items may vary among analysts. There is no single universally accepted method for every scenario, so transparency about what is included in EBITDA is essential. Tools like Econblox’s AI-powered business advisor can help owners pressure-test their assumptions and interpret a multiple within the context of their own industry.

Frequently Asked Questions

What is a good EBITDA multiple for my business?

There is no universal good multiple. It depends on your industry, growth prospects, profitability, and company size. For a broad reference, some public companies trade around 8x EV/EBITDA, but Aerospace & Defense averaged 15.78x in 2026 while Broadcasting averaged only 2.76x. Compare against direct industry peers.

How do I calculate Last Twelve Months (LTM) EBITDA?

LTM EBITDA blends the most recent stub period with the latest full fiscal year. Add the EBITDA from the most recent stub period to the latest full-year EBITDA, then subtract the EBITDA from the corresponding prior stub period. This avoids counting the same months twice and gives a clean trailing figure.

What is the difference between EV/EBITDA and EBITDA/EV?

EV/EBITDA is enterprise value divided by EBITDA; it is the standard valuation multiple. EBITDA/EV is the reciprocal, EBITDA divided by enterprise value, and it measures the cash return on enterprise value. A higher EBITDA/EV means more operating cash for each dollar of enterprise value.

Is EBITDA the same as cash flow?

No. EBITDA is a non-GAAP proxy for operating cash flow, but it ignores changes in working capital, capital expenditures, and other cash items. For a more accurate cash flow view, you would need to calculate free cash flow. EBITDA is best used for quick comparisons and valuation multiples, not as a precise cash flow measure.

Understanding how to calculate your EBITDA multiple gives you a powerful tool for benchmarking your business against peers and for preparing for a potential sale or investment. The math is straightforward: divide enterprise value by EBITDA. The challenge is getting both numbers right and interpreting the result within your industry’s normal range. With the formulas and context provided here, you can begin your own EBITDA multiple calculation with confidence. Of all the risks checked during due diligence, high owner dependency business valuation is the most common multiple compressor. Understanding your margin erosion causes is equally critical — any operational leaks directly reduce your EBITDA baseline. If a buyer spots significant customer concentration risk, they will apply a steep discount to your multiple. Avoid the growth trap business cycle — top-line expansion at the expense of profitable margins destroys the multiple you are trying to build.

No Credit Card Required For Trial

No Credit Card Required For Trial