When you operate a business that relies heavily on a small number of customers, that dependency is a central factor in valuation. Buyers and auditors evaluate customer concentration as a key risk indicator, often adjusting pricing and audit fees accordingly. Conducting a customer concentration audit on your own terms gives you the opportunity to understand and address that risk before an outside party raises it. This article explains what a customer concentration audit involves, why it matters for both financial reporting and exit planning, and how to perform one effectively using established benchmarks and research findings.

What Is a Customer Concentration Audit?

A customer concentration audit is a systematic review of how much of your total revenue depends on a limited set of customers. The goal is to identify concentration levels that could signal business vulnerability, raise audit fees, or reduce exit value. Different sources define concentration thresholds differently, so it helps to compare them. The advisory firm Kreischer Miller (KMCO), in an August 2015 article, defines customer concentration as a single customer or group of customers accounting for 8% or more of total sales. Allianz Trade, in a more recent article on avoiding high customer concentration risk, defines high concentration as any single customer representing 20% or more of total revenue. Private equity firm Montage Partners places the “high concentration” line a bit higher still, at 25% to 30% of revenue from one customer, while noting that a long-standing contract or a sole-provider position can offset some of that risk in a buyer’s eyes. No single standard is universally accepted, but using these ranges gives you a practical framework for evaluating your own exposure.

Why Customer Concentration Concerns Buyers and Auditors

Customer concentration is a red flag for buyers because it signals revenue instability, and it is one of the factors buyers use to discount a purchase price. If one customer walks away, the business takes a significant hit. But the concern also extends to auditors, who must weigh the risk of material misstatement and going concern issues. Research published in the Managerial Auditing Journal in 2021 by Chen and colleagues found that governmental customer concentration is positively associated with audit fees, indicating that auditors perceive higher risk and exert more effort when a large portion of revenue comes from government entities. That finding runs the opposite direction from customer concentration generally: a separate study by Eshleman and colleagues in the Journal of Accounting and Finance in 2018 found that broader customer-base concentration is associated with lower audit fees, consistent with auditors gaining efficiency when a client’s revenue and controls are easier to trace to a small number of large accounts.

Financial Reporting Quality and Restatements

Not all effects of customer concentration are negative from a reporting standpoint. Research published in the Journal of Management Accounting Research (AAAHQ) in March 2019 similarly found that customer-base concentration is associated with both lower audit fees and a lower likelihood of material restatements of previously issued financial statements. This suggests that when a business depends on a few large customers, management may be more cautious about revenue recognition and disclosure. However, that reporting stability does not eliminate the underlying business risk. A buyer evaluating your company will weigh the lower restatement risk against the higher customer dependency risk, and an auditor may still increase audit effort and fees based on the concentration level, particularly if any of those customers are governmental.

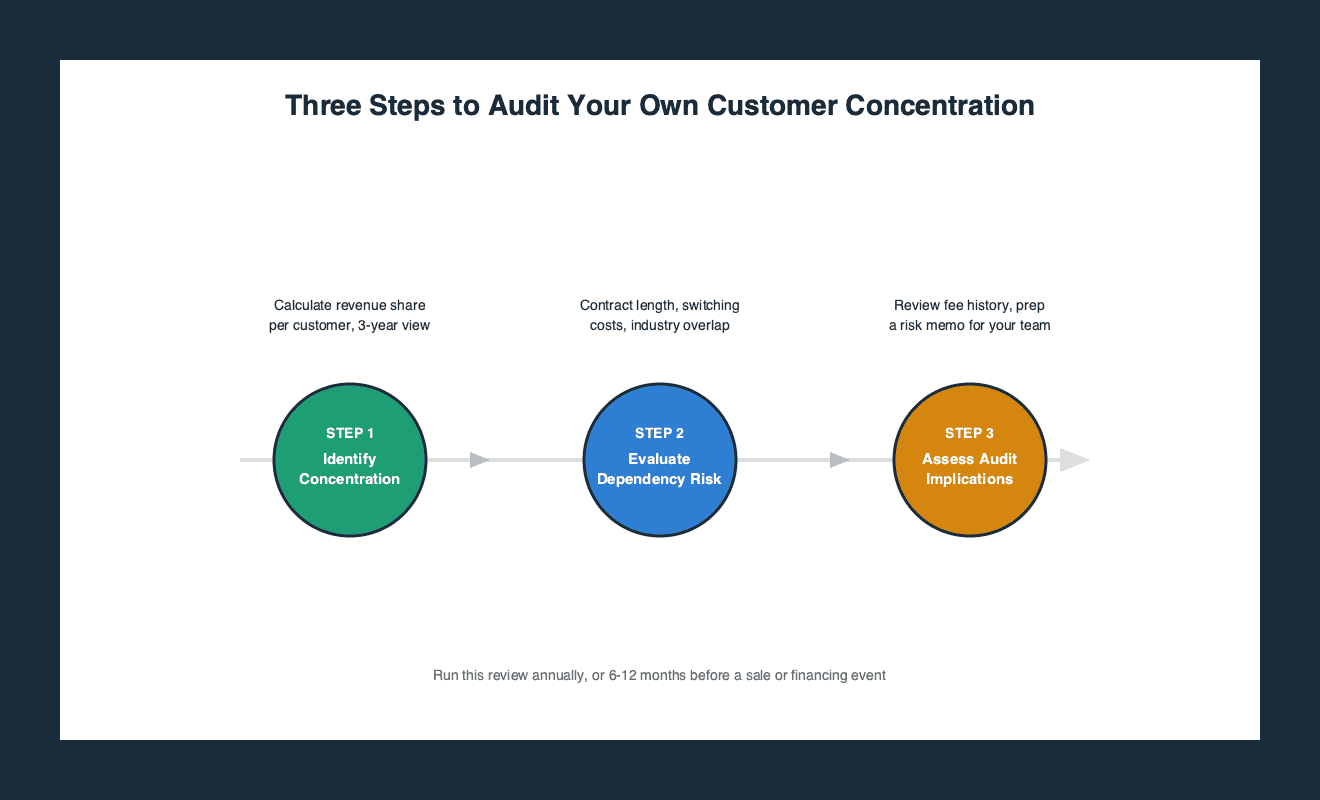

How to Perform Your Own Customer Concentration Audit

Performing your own audit puts you in control of the narrative. You can identify issues, document mitigation plans, and present a stronger case to buyers and auditors. Follow these steps to conduct a thorough review.

Identify Your Revenue Concentration

Gather your revenue data for at least the past three fiscal years. Calculate the percentage of total sales attributable to each customer and to the top five customers collectively. Compare your figures against three thresholds: 10%, 20%, and 30%. Flag any customer that exceeds any of these benchmarks.

Evaluate Customer Dependency Risk

Concentration numbers alone do not tell the full story. Assess the nature of each concentrated relationship. Consider the length of the customer contract, the switching costs for the customer to leave, the financial health of that customer, and whether the revenue is from repeat purchases or one time projects. Also examine whether the concentrated customers operate in the same industry or geographic region. If your top customers share a common industry, you face not only customer concentration risk but also industry risk. Contracts with long terms and high switching costs reduce risk, while short term or at will agreements increase it.

Assess Audit Implications

Review how your auditor has treated customer concentration in past engagements. Look at prior year audit fee disclosures and any management letter comments about revenue concentration. If you have governmental customers, the Chen et al. 2021 research suggests auditors may charge higher fees. For non-governmental concentration, the Eshleman et al. 2018 and Krishnan et al. 2019 studies point the other way on fees, though the underlying business risk of depending on a few large customers remains. Prepare a memo that documents your understanding of the risk and any mitigating controls you have in place, such as customer diversification initiatives or long term contract provisions. This memo can be shared with your audit team to reduce surprise fee increases and to demonstrate proactive governance.

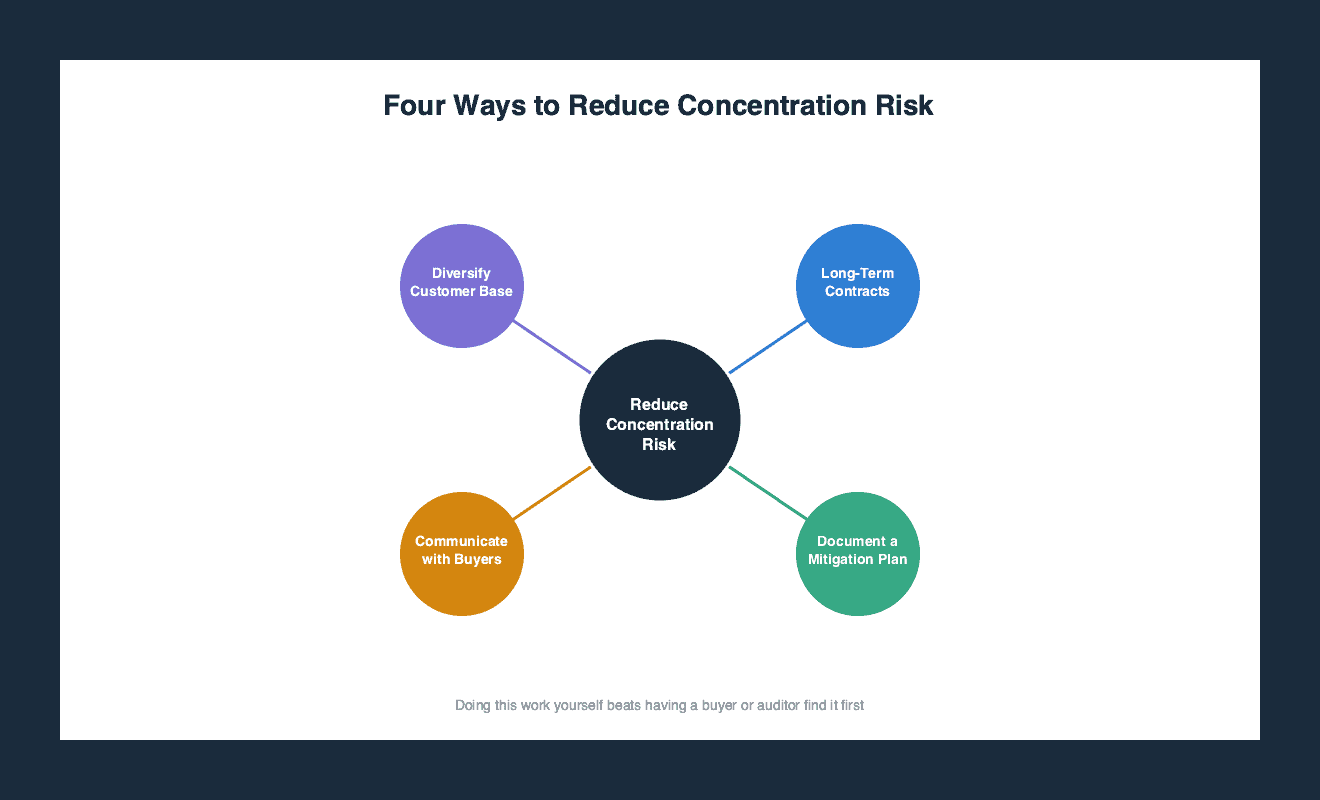

Taking Action on Your Findings

Once you have completed your audit, the next step is to act on the results. Ignoring high concentration leaves you vulnerable to reduced business valuation and higher audit costs. Here are two practical areas to address.

Diversification Strategies

If your audit reveals excessive concentration, develop a plan to broaden your customer base. Target new industries or geographic regions that align with your capabilities. Invest in sales and marketing to cultivate additional accounts that can each contribute a meaningful but non dominating share of revenue. Consider strategic alliances or partnerships that bring in complementary customer streams. For existing concentrated customers, negotiate longer contract terms or volume commitments that lock in revenue for a set period. Even partial diversification can shift the concentration ratio enough to move below the key thresholds and reduce audit risk.

Communicating with Potential Buyers

When you approach the market to sell your business, a proactive customer concentration audit gives you an advantage. Prepare a summary of your concentration analysis, highlighting any mitigating factors such as contract length, customer retention history, and diversification efforts. If you have reduced concentration over time, show the trend. If concentration remains high, be transparent about the steps you take to manage the risk, such as maintaining a pipeline of potential replacement customers or having a transition plan in the event of customer loss. Buyers are more comfortable when you have already done the work they would otherwise do themselves.

Frequently Asked Questions

What percentage of revenue from one customer is considered high concentration?

There is no single universal threshold, but common benchmarks include 8% of total sales (Kreischer Miller), 20% of revenue (Allianz Trade), and 25% to 30% (Montage Partners). The most frequently cited definition in general business contexts is 20% or more from one customer, which Allianz Trade identifies as high concentration.

Does customer concentration always increase audit fees?

No. Research shows a positive association between governmental customer concentration and higher audit fees (Chen et al. 2021), but broader, non-governmental customer-base concentration has been linked to lower audit fees in two separate studies (Eshleman et al. 2018; Krishnan et al. 2019), consistent with auditors gaining efficiency rather than facing more risk. The relationship depends on the type of customer, the audit firm, and the specific risk factors present.

Can customer concentration ever be beneficial for a business?

Yes. Research published in the Journal of Management Accounting Research in 2019 found that customer-base concentration is associated with a lower likelihood of material restatements. Concentrated revenue can also lead to stable, predictable cash flows and deeper customer relationships. The challenge is balancing those benefits against the risk of dependency.

How often should I conduct a customer concentration audit?

At minimum, perform the audit annually as part of your financial planning process. If you are preparing for a sale or a major financing event, conduct an additional audit six to twelve months before the transaction. Any significant change in your customer base, such as losing a major account or winning a very large new one, should trigger an immediate review. The diagnostic results of this assessment will show you exactly how to diversify customer base revenue streams safely. For complete operational security, analyze supplier reliance side-by-side with a vendor dependency risk evaluation. Failing to act on concentration data is one of the most common hidden margin erosion causes in mid-market businesses.

No Credit Card Required For Trial

No Credit Card Required For Trial