A healthy business can look strong on paper, with growing revenue and a loyal client base. But if too much of that revenue comes from a single customer or a small group of customers, the company may be sitting on a hidden vulnerability. This vulnerability is known as customer concentration risk, and it can destabilize even the most promising enterprises. When a major client reduces spending, switches suppliers, or goes out of business, the financial shock can be severe. Understanding and monitoring customer concentration is essential for any business owner who wants to build sustainable, resilient operations.

What Is Customer Concentration Risk?

Customer concentration risk is the risk that stems from a company’s revenue being too reliant on a small subset of customers. When a large share of revenue depends on a small number of customers, the business becomes vulnerable to the loss or reduction of those accounts. Customer concentration happens when a large share of a company’s revenue depends on a small number of customers. This creates financial risk if those customers reduce their spend or leave entirely.

Customer concentration is typically measured as the percentage of total revenue from a company’s top customer or group of customers. For example, Nvidia’s 10-Q filing for the quarter ended April 26, 2026 disclosed that three unnamed direct customers accounted for a combined 64% of total revenue. While Nvidia’s situation may be unique given its market position, such a high concentration would alarm most investors and lenders. For a closer look at how this factors into Nvidia’s competitive position, see our analysis of Nvidia’s demand and competitive dynamics. The risk is not hypothetical. Over 40% of listed firms in China have at least one major customer that represents more than 10% of sales, compared to just 8% of listed firms in the United States, according to a 2021 study in the Journal of Financial Stability by Cao et al. That same study found that overall customer concentration significantly reduces corporate risk-taking, though the relationship shows threshold effects, meaning low concentration levels can be positively associated with risk-taking while high levels turn negative.

How Much Customer Concentration Is Too Much?

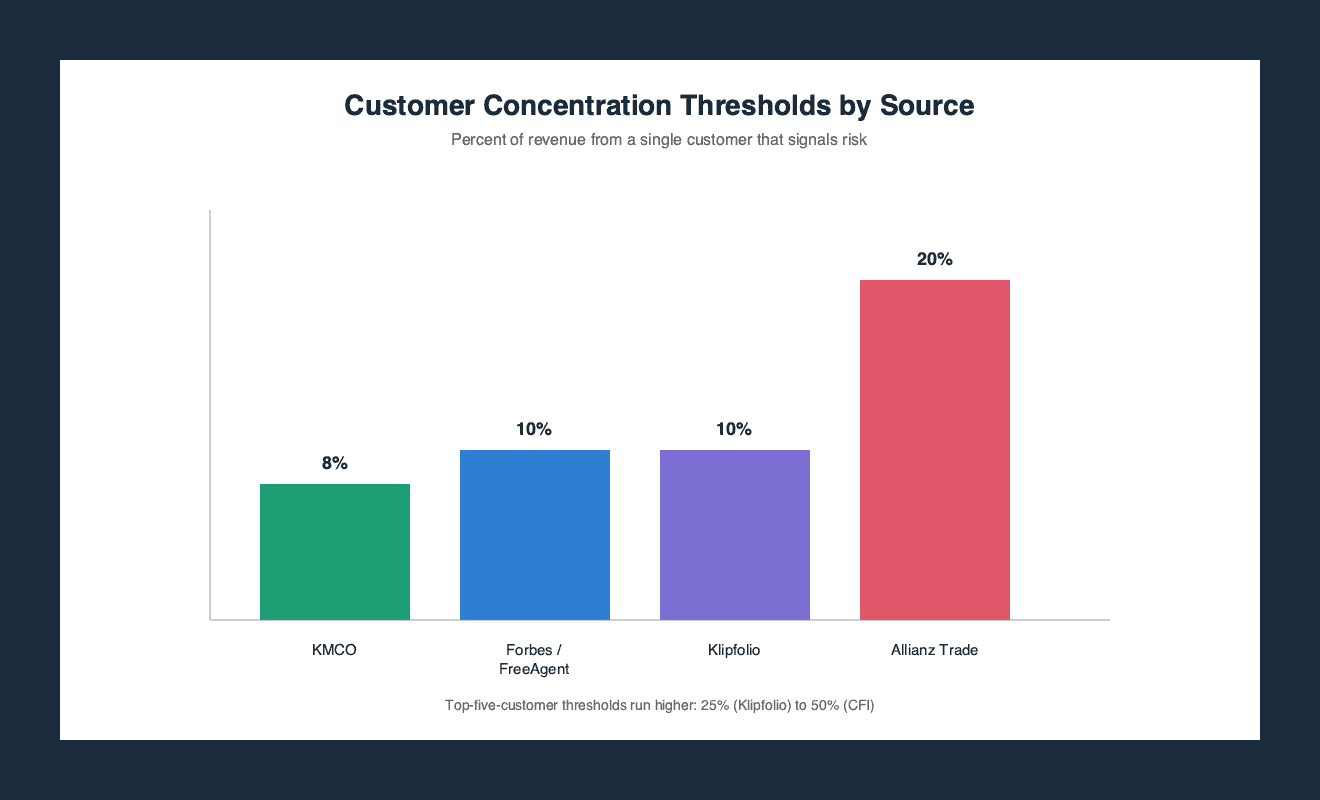

There is no universally accepted single threshold that defines high customer concentration risk. Different sources recommend different benchmarks, and the right level varies by industry, business model, and growth stage. Business owners should be aware of the various guidelines and evaluate their own exposure relative to their specific context.

| Source | Threshold | Notes |

|---|---|---|

| KMCO | 8% of total sales from a single customer or group | One common definition used by risk analysts |

| Forbes (via FreeAgent) | 10% of revenue from a single client | As little as 10% may put a business at risk |

| Klipfolio | 10% from one client, or 25% from top five | Indicates high customer concentration |

| Allianz Trade | 20% or more of revenue from a single customer | Defines high concentration |

| CFI | Top five customers account for more than 50% | Defines high concentration |

As the table shows, the thresholds range from a conservative 8% to a more lenient 50% for the top five customers. This lack of a single standard means business owners must use judgment. A startup with a single anchor client may accept higher concentration temporarily, while a mature firm with multiple revenue streams should aim for lower numbers. The key is to be aware of the risk and to monitor changes in customer dependence over time.

The Real Impact of Customer Concentration

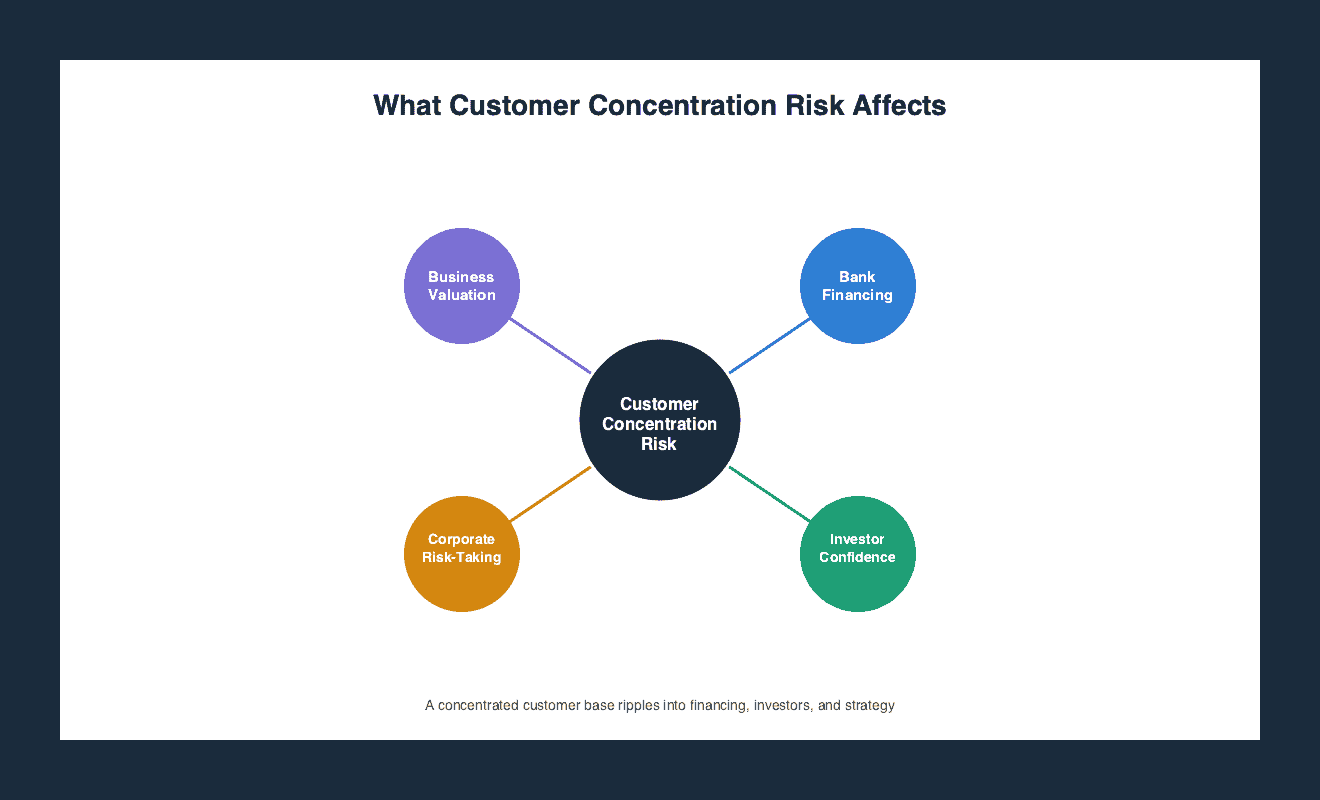

High customer concentration risk has tangible consequences beyond the obvious danger of losing a major client. It can directly affect business valuation, access to bank financing, and investor confidence. Banks and investors view a concentrated customer base as a red flag because it signals fragility. A company that depends on one or two large accounts is seen as less predictable and more likely to suffer sudden revenue drops.

Valuation multiples often compress for firms with high customer concentration. Buyers and acquirers discount the perceived risk, offering lower prices, consistent with the broader set of factors buyers use to discount a purchase price. Similarly, lenders may impose stricter terms or higher interest rates, or may decline financing altogether. The Cao et al. research also indicates that overall customer concentration reduces corporate risk-taking, which can constrain growth. However, the same study found that at low concentration levels, the relationship with risk-taking can be positive. This suggests a nuanced picture: some dependence on key customers may be beneficial up to a point, but crossing a certain threshold flips the effect to negative.

For a business owner, this means that moderate customer concentration might be acceptable during growth phases, but ignoring the risk as revenue scales can become dangerous. The threshold effect reinforces the importance of measuring and managing concentration proactively.

Customer Concentration Across Markets

The prevalence of customer concentration varies significantly by market and regulatory environment. Research comparing listed firms in China and the United States found that over 40% of Chinese firms had at least one major customer representing more than 10% of sales, compared to just 8% of U.S. firms. This stark difference may reflect different supply chain structures, regulatory disclosure requirements, or economic models. For U.S. business owners, the lower average concentration is a reminder that American markets generally expect more diversified revenue bases. For companies operating internationally or dealing with Chinese partners, understanding these norms is important for risk assessment.

The difference also suggests that customer concentration risk is not merely a matter of company size or industry. Structural factors in the broader economy play a role. Business owners should benchmark their own concentration not just against generic guidelines but against peers in their sector and region.

Managing Customer Concentration Risk

While the research pack does not detail specific mitigation strategies that are universally effective, business owners can take several general steps to reduce customer concentration risk. Diversifying the customer base is the most direct approach. This may involve expanding into new geographic markets, targeting different customer segments, or developing new products and services that appeal to a broader audience. Another approach is to negotiate longer-term contracts or retainers with major customers to increase revenue visibility and reduce the probability of sudden loss.

Building a strong sales pipeline and continuously prospecting for new clients helps ensure that no single customer represents an outsized share of revenue. Financial reserves, such as a cash buffer, can provide a cushion if a major client does leave. Regular monitoring of concentration metrics, using the thresholds discussed earlier, allows business owners to spot trends before they become crises. Tools like Econblox’s AI-powered business advisor can help track these metrics on an ongoing basis rather than discovering a problem after it has already grown. Finally, being transparent with investors and lenders about customer concentration and having a plan to address it can mitigate the negative impact on valuation and financing.

It is important to note that the effectiveness of any specific strategy depends on the business context. A company that can maintain close, strategic relationships with a few large customers while still diversifying overall may achieve a healthy balance. The goal is not zero concentration but controlled and manageable exposure.

Frequently Asked Questions

What percentage of revenue from one customer is considered too high?

There is no single standard. Various sources use thresholds ranging from 8% to 20% for a single customer, and up to 50% for the top five customers. A common warning sign is when one client accounts for 10% or more of revenue. Business owners should evaluate their own risk tolerance and industry norms.

How does customer concentration risk affect business valuation?

High customer concentration risk can reduce business valuation because buyers and investors see it as a weakness. A company overly dependent on one or a few customers is considered less stable and more likely to experience sudden revenue loss. This often leads to lower valuation multiples and stricter financing terms.

Can customer concentration ever be a positive thing?

Yes, at low levels. Research shows that some customer concentration can be positively associated with corporate risk-taking, likely because close relationships with key customers provide stability and enable investment. However, when concentration crosses a certain threshold, the effect turns negative and overall risk-taking declines.

Is customer concentration risk only a problem for small businesses?

No. Large corporations can also face this risk. For example, Nvidia disclosed that three customers accounted for 64% of its revenue in its 10-Q filing for the quarter ended April 26, 2026. Any business, regardless of size, can be vulnerable if revenue is too dependent on a small number of accounts.

Customer concentration risk is a quiet but powerful threat that can undermine a healthy business. By understanding the definition, measuring exposure against the various thresholds, and taking proactive steps to diversify revenue, business owners can protect their companies from the shock of losing a major client. Regular monitoring and strategic planning turn this hidden vulnerability into a managed risk, supporting long-term stability and growth. To defend your margins, build a programmatic framework to diversify customer base revenue streams safely. Before making major strategic moves, establish your current threat level by executing a formal customer concentration audit. You must also secure your supply chain against severe vendor dependency risk variables. You will only find the leverage to protect margins once you build the power to raise prices without losing customers. Managing expansion budgets carefully also prevents stepping into a classic growth trap business cash flow crisis.

No Credit Card Required For Trial

No Credit Card Required For Trial