Smart Retirement Planning for Small Business Owners

For many established business owners, the company they built represents far more than an income stream. It often becomes their primary retirement plan. The logic seems sound: grow the business, increase its value, and eventually sell it or draw enough income to fund retirement.

But this approach carries significant risk. A market downturn, industry disruption, or a key employee departure can severely impact the business’s value, leaving the owner with a much smaller nest egg than expected.

The alternative is to build retirement savings inside the business itself, separate from the enterprise’s operating capital. Fortunately, several retirement plan options allow business owners to save on a tax-deferred basis, effectively creating a pension funded by their own company.

Why Relying on Your Business as Your Pension Is Risky

Treating a business as a pension assumes that the business will always be salable at a high multiple, or that the owner can keep drawing salary indefinitely. Neither assumption is guaranteed. Business values fluctuate based on economic conditions, and an owner’s ability to sell often depends on finding a qualified buyer or successor. Furthermore, if the business hits a rough patch, the owner may be forced to sell at a discount or retire later than planned.

By contrast, a dedicated retirement plan provides a separate pool of assets that grows regardless of the company’s fortunes. This separation gives the owner options. Even if the business is sold for less than expected, the retirement plan remains intact. Tax-deferred growth also means more compounding inside the plan. It also helps insulate the owner from broader macro pressures, such as rising government debt and its effect on retirement savings, that can weigh on both business value and personal investments at the same time.

For these reasons, financial advisors and tax professionals encourage business owners to treat retirement contributions as a non-negotiable expense, just like payroll or rent. If you are unsure whether your current approach holds up, it helps to review the warning signs that a retirement plan wasn’t built for this economy before a downturn forces the issue.

Retirement Plan Options for Self-Employed Business Owners

The IRS provides several plan types designed specifically for self-employed individuals and small business owners. These plans allow contributions to be made on a tax-deferred basis, reducing current taxable income while building retirement savings.

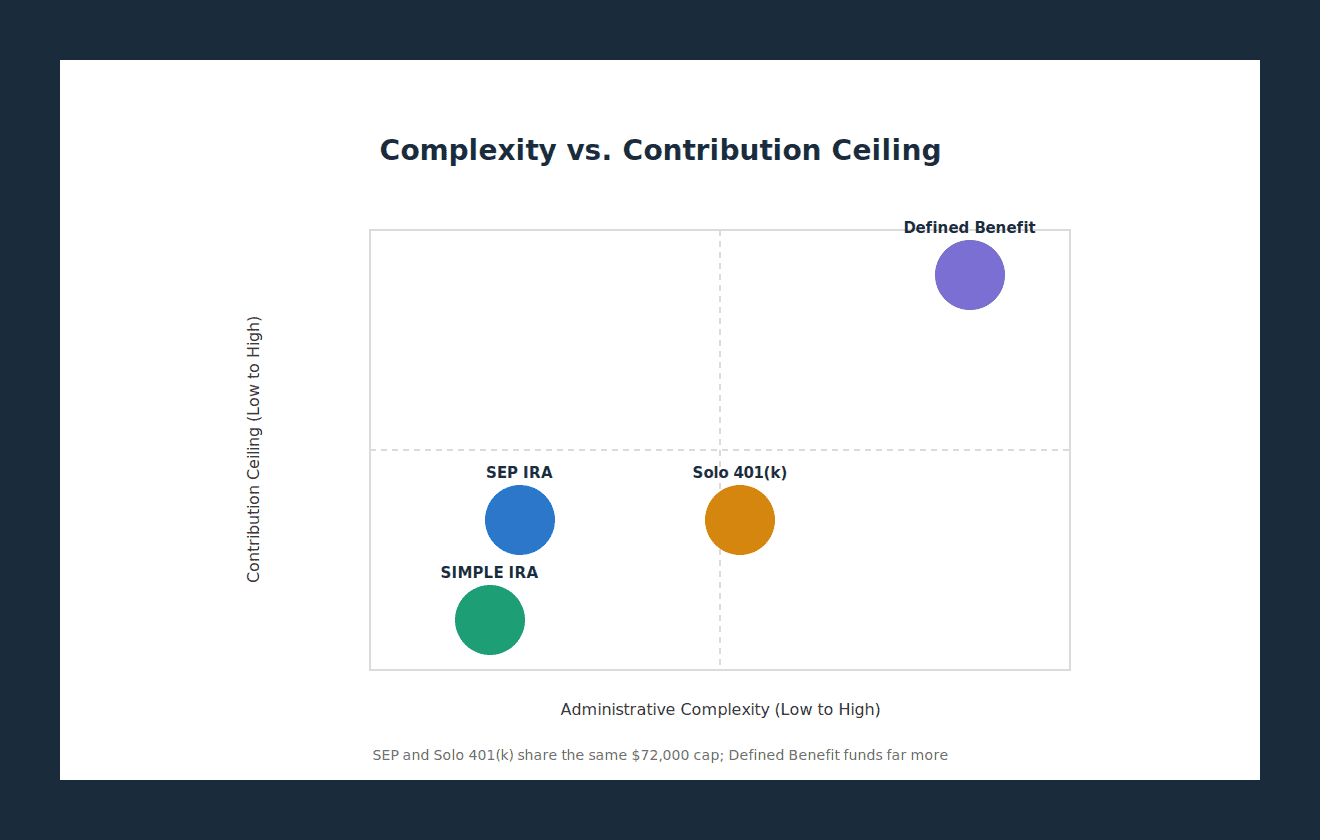

The four most common options are SEP IRAs, Solo 401(k)s, SIMPLE IRAs, and Defined Benefit Plans. Each has distinct contribution limits, eligibility rules, and administrative requirements.

SEP IRA (Simplified Employee Pension)

A SEP IRA is one of the simplest retirement plans to set up and maintain. It uses IRS Form 5305-SEP, a one-page document. Contributions are made only by the employer, not by employees.

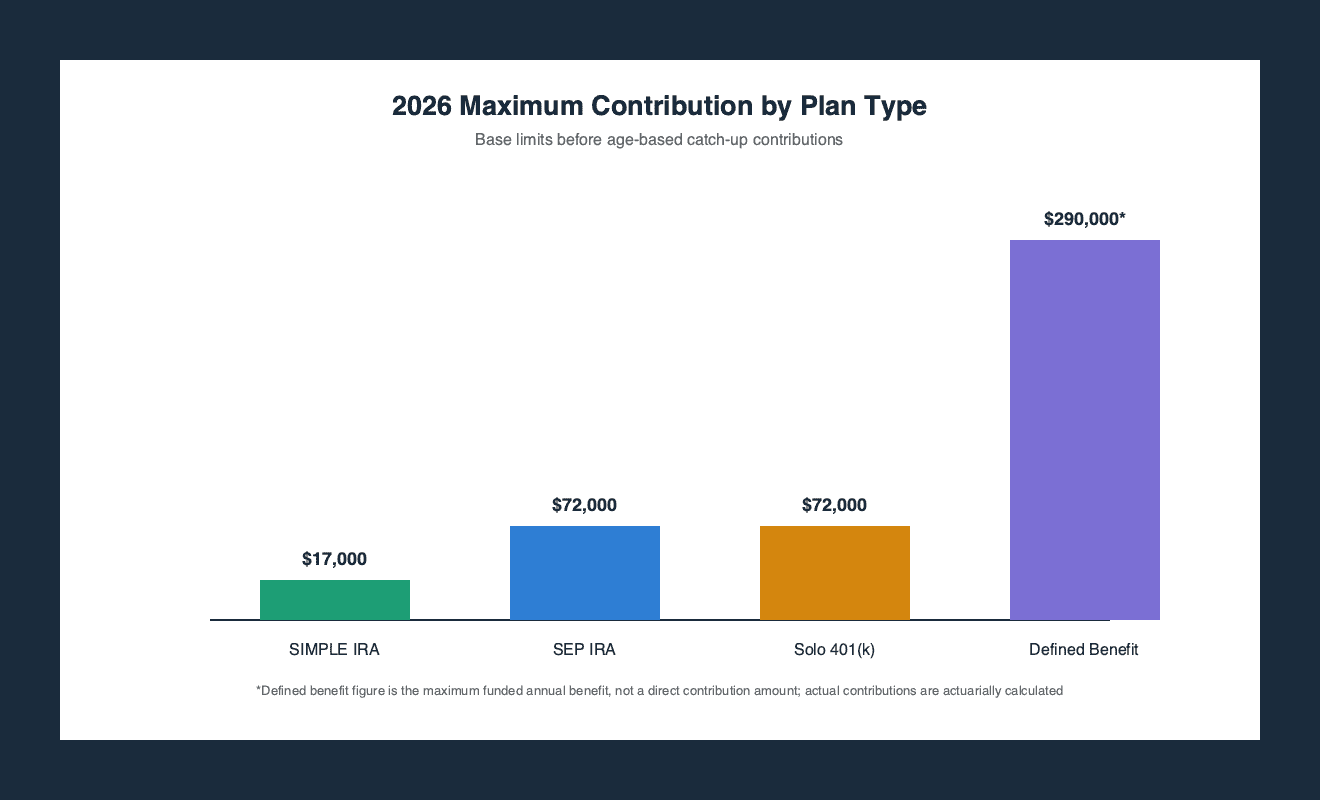

For 2026, the maximum contribution limit is up to 25% of net earnings from self-employment, capped at $72,000 (up from $69,000 in 2024 and $70,000 in 2025). SEP IRAs are typically used by sole proprietors or businesses with up to four employees, though the IRS allows any size business to adopt one.

Because the employer must contribute the exact same percentage of salary for all eligible employees, it becomes less attractive if the owner wants to maximize contributions for themselves but cannot afford to do so for their staff. There is no nondiscrimination testing requirement, and no Form 5500 filing is needed. For an owner-only business with no employees other than a spouse, a SEP IRA offers a straightforward way to save a large portion of income.

Solo 401(k) (Individual 401(k))

The Solo 401(k), also called an Individual 401(k), is designed specifically for owner-only businesses with no employees except a spouse. It allows both employee salary deferrals and employer profit-sharing contributions.

For 2026, the individual elective deferral limit is $24,500, plus a standard catch-up contribution of $8,000 for those age 50 or older. Total contributions (employee plus employer) are capped at $72,000. Under the SECURE 2.0 Act, a special “super catch-up” limit of $11,250 applies to plan participants aged 60 to 63, allowing them an alternative employee deferral cap of $35,750.

Solo 401(k)s can include a Roth option for post-tax savings and offer very high contribution limits for solo operators. Crucially, because a Solo 401(k) only covers the business owner and their spouse, it is entirely exempt from IRS nondiscrimination testing. However, they do require an annual Form 5500 filing once total plan assets exceed $250,000.

SIMPLE IRA

The SIMPLE IRA (Savings Incentive Match Plan for Employees) is intended for businesses with 100 or fewer employees that do not sponsor another retirement plan. For 2026, employees can defer up to $17,000, plus a $4,000 catch-up for those 50 or older.

Employers must either make a 2% fixed contribution to all eligible employees or match employee deferrals dollar-for-dollar up to 3% of compensation. The employer contribution is fully tax-deductible.

SIMPLE IRAs are completely exempt from nondiscrimination testing and do not require Form 5500 filing. Because the contribution limits are lower than those of a 401(k) or SEP IRA, this plan is best suited for businesses that want a low-cost, low-hassle option while still providing a basic retirement benefit to employees.

Defined Benefit Plans (Traditional or Cash Balance)

For business owners who want to contribute the largest possible amount and are willing to accept more complexity, a defined benefit plan is the ultimate tool. Instead of defining what goes into the plan, these plans promise a specified monthly benefit at retirement, usually based on age, salary, and years of service.

For 2026, the maximum annual benefit that can be funded and provided is $290,000 (up from $275,000 in 2024). Because contributions are actuarially calculated to meet that target, annual tax-deductible contributions can easily exceed $100,000 to $200,000+ depending on the owner’s profile. This allows for vastly higher annual contributions than any 401(k) or SEP IRA.

However, these plans come with significant administrative burdens, including annual actuarial certifications, nondiscrimination testing (if non-spouse employees are present), and mandatory annual Form 5500 filings. Many major brokerages offer scaled-down versions of these plans tailored for owner-only businesses or businesses with fewer than five employees. These plans are ideal for highly profitable, older business owners who need to accelerate their retirement savings significantly in the years immediately preceding retirement.

Comparing Plan Types: Contribution Limits and Requirements (2026 Data)

| Plan Type | 2026 Employee Deferral Limit | 2026 Total Contribution Limit | Employer Only? | Nondiscrimination Testing? | Form 5500 Required? |

|---|---|---|---|---|---|

| SEP IRA | N/A (Employer Only) | 25% of compensation, up to $72,000 | Yes | No | No |

| Solo 401(k) | $24,500 ($32,500 with catch-up; $35,750 if age 60-63) | $72,000 | No (Both sides) | No | Only if plan assets >$250,000 |

| SIMPLE IRA | $17,000 ($21,000 with catch-up) | Deferral amount + Employer match | No (Both sides) | No | No |

| Defined Benefit Plan | N/A (Employer Only) | Actuarial calculation (Funds an annual benefit up to $290,000) | Yes | Yes (If employees exist) | Yes |

As shown, defined benefit plans allow for the largest overall contributions, while Solo 401(k) plans offer the highest limits among the standard defined contribution accounts. SEP IRAs are simpler but have lower effective limits for business owners with fluctuating net self-employment income. SIMPLE IRAs work best for businesses with many employees but limited benefit budgets.

Administrative Considerations for Business Owners

Choosing a retirement plan involves more than just contribution limits; administrative burden is a key deciding factor.

SEP IRAs and SIMPLE IRAs are the easiest to maintain. They are exempt from nondiscrimination testing and do not require an annual Form 5500 filing. SEP IRAs use a simple one-page IRS form (Form 5305-SEP) to establish the plan, while SIMPLE IRAs require minimal ongoing paperwork. Both are popular with small business owners who want to completely avoid operational complexity.

In contrast, Solo 401(k) plans bridge the gap, requiring a Form 5500 only when assets hit the $250,000 milestone, while avoiding testing entirely. Defined benefit plans carry the highest administrative costs because they require actuarial valuations every single year and must file complex Form 5500 schedules with detailed participant asset tracking.

Business owners should also consider that provider fees vary widely. Some digital-first brokerages charge no fees to open or maintain basic SEP or SIMPLE IRAs, while standard 401(k) and defined benefit plans generally carry higher annual maintenance and document fees.

Tax Benefits of Business Retirement Plans

Employer contributions to a retirement plan are generally tax-deductible for the business. This directly reduces the company’s taxable income, providing an immediate cash flow benefit. Employee deferrals in a traditional 401(k) or SIMPLE IRA are made pre-tax, lowering the employee’s personal income tax liability for the year.

Earnings in all these plans grow on a tax-deferred basis, meaning no taxes are due until money is withdrawn in retirement. This allows compounding to work much more efficiently. For business owners who expect to be in a lower tax bracket in retirement, the tax deferral can be highly advantageous.

Additionally, plans like the Solo 401(k) offer a Roth option, where contributions are made after-tax but qualified withdrawals in retirement are entirely tax-free. Balancing pre-tax and Roth allocations, alongside outside investments such as a traditional stock-and-bond portfolio, can help business owners manage their lifetime tax exposure and avoid concentrating all their savings in a single strategy.

For business owners whose primary retirement asset is the business itself, these tax-advantaged plans work best as a complement to a planned exit. Transforming your business from an illiquid asset into actual cash requires a rigorous exit prep checklist business owners can execute over several years. That process starts with knowing your number — a formal business valuation for owners is the foundation of any credible retirement plan built around a business sale. In the years leading up to exit, your most powerful lever is margin discipline: demonstrating the ability to raise prices without losing customers directly compounds your cash flow and your exit multiple.

Frequently Asked Questions

What is the difference between a SEP IRA and a SIMPLE IRA?

A SEP IRA allows employer-only contributions of up to 25% of compensation, capped at a dollar limit that adjusts annually ($72,000 for 2026). A SIMPLE IRA allows both employee salary deferrals ($17,000 for 2026) and mandatory employer contributions (either a 2% fixed contribution or a 3% match). SIMPLE IRAs are designed for businesses with up to 100 employees, while SEP IRAs can be used by any size business. Contribution limits are generally higher under SEP IRAs for high earners, but SEP IRAs require the employer to contribute the same percentage for staff as they do for themselves.

How much can I contribute to a Solo 401(k) in 2026?

For 2026, the employee salary deferral limit is $24,500, plus an $8,000 catch-up for those age 50 or older (or an $11,250 catch-up for ages 60 to 63). Total contributions, including the employer profit-sharing contribution, cannot exceed $72,000. These limits apply strictly to owner-only businesses with no employees other than a spouse.

Do I need to file Form 5500 for a SEP IRA?

No. SEP IRAs are completely exempt from the annual Form 5500 filing requirement, regardless of how large the plan assets grow. SIMPLE IRAs are also exempt. This makes both plans significantly simpler to administer than a Solo 401(k), which must begin filing Form 5500-SF once total plan assets cross $250,000. However, if you adopt a SEP IRA, you must permanently retain your executed Form 5305-SEP and all annual records of employer contributions.

No Credit Card Required For Trial

No Credit Card Required For Trial